Page 232 - BTSGroup ONE REPORT 2021/22_EN

P. 232

230 l Introduction l Nature of Business l Organisation and Shareholding Structure l Business Review l Corporate Governance l Financial Statements l Other Information l

the pooled entities are directly recognised in shareholders’ equity (and The Group as a lessee

if the pooled entities have profit or loss transactions directly recognised The Group applied a single recognition and measurement approach for

in the shareholders’ equity, the financial statements after business all leases, except for short-term leases and leases of low-value assets.

combination present the transaction as if the business combination At the commencement date of the lease (i.e. the date the underlying

occurred at the earliest reporting date). The remaining difference between asset is available for use), the Group recognises right-of-use assets

the cost of the business combination under common control and the representing the right to use underlying assets and lease liabilities based

acquirer’s proportionate interest in the book value the pooled entities, on lease payments.

after recognising the profit or loss transactions directly in shareholders’

equity, is presented as “Surplus (deficit) on business combination under Right-of-use assets

common control” in shareholders’ equity.

Right-of-use assets are measured at cost, less accumulated depreciation,

Costs relating to business combinations under common control any accumulated impairment losses, and adjusted for any remeasurement

are accounted for as expenses in the period in which the business of lease liabilities. The cost of right-of-use assets includes the amount

combination occurred. of lease liabilities initially recognised, initial direct costs incurred,

and lease payments made at or before the commencement date of the lease

4.17 Borrowing costs and an estimate of costs to dismantle and remove the underlying asset

or to restore the underlying asset or the site on which it is located less

Borrowing costs directly attributable to the acquisition, construction or any lease incentives received.

production of an asset that necessarily takes a substantial period of time

to get ready for its intended use or sale are capitalised as part of the Depreciation of right-of-use assets are calculated by reference to their

cost of the respective assets. All other borrowing costs are expensed costs, on the straight-line basis over the shorter of their estimated useful

in the period they are incurred. Borrowing costs consist of interest lives and the lease term.

and other costs that an entity incurs in connection with the borrowing

of funds.

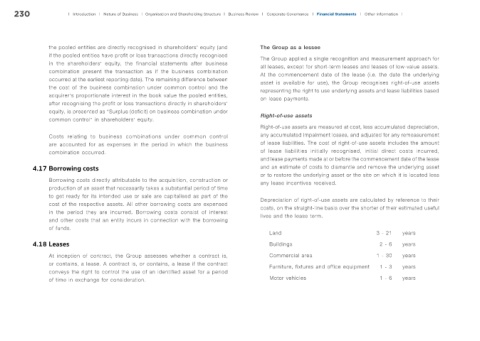

Land 3 - 21 years

4.18 Leases Buildings 2 - 6 years

At inception of contract, the Group assesses whether a contract is, Commercial area 1 - 30 years

or contains, a lease. A contract is, or contains, a lease if the contract Furniture, fixtures and office equipment 1 - 3 years

conveys the right to control the use of an identified asset for a period

of time in exchange for consideration. Motor vehicles 1 - 6 years